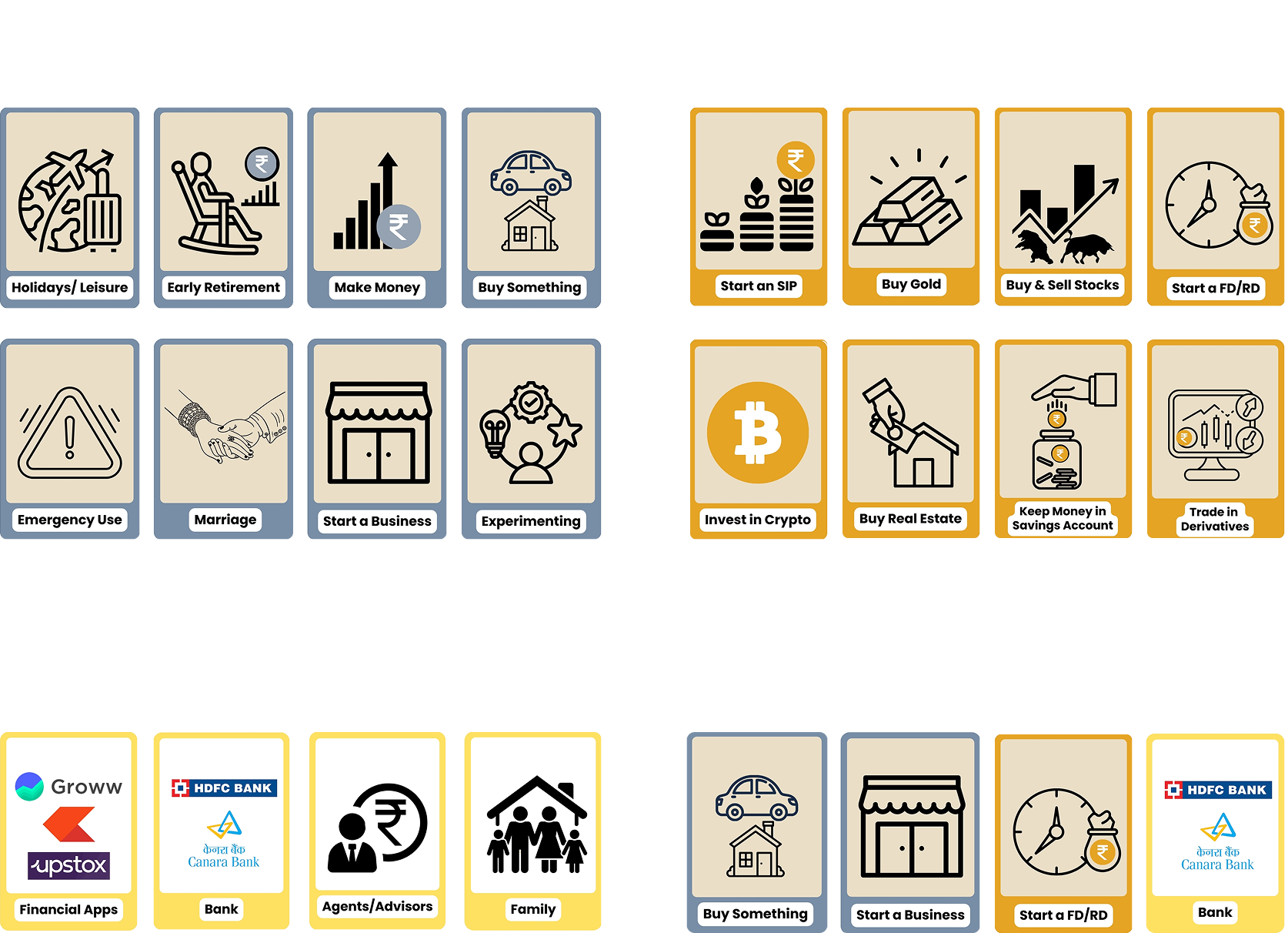

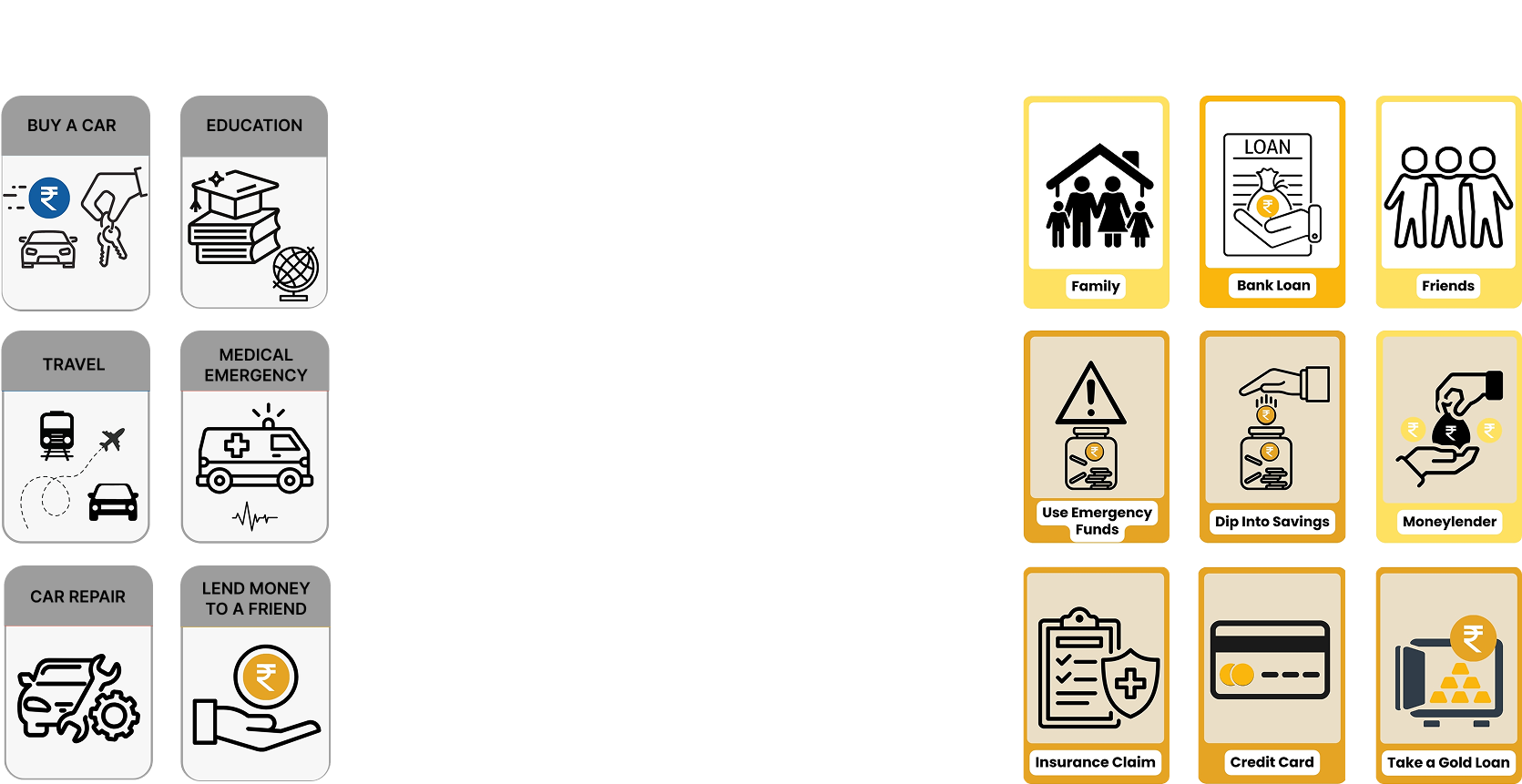

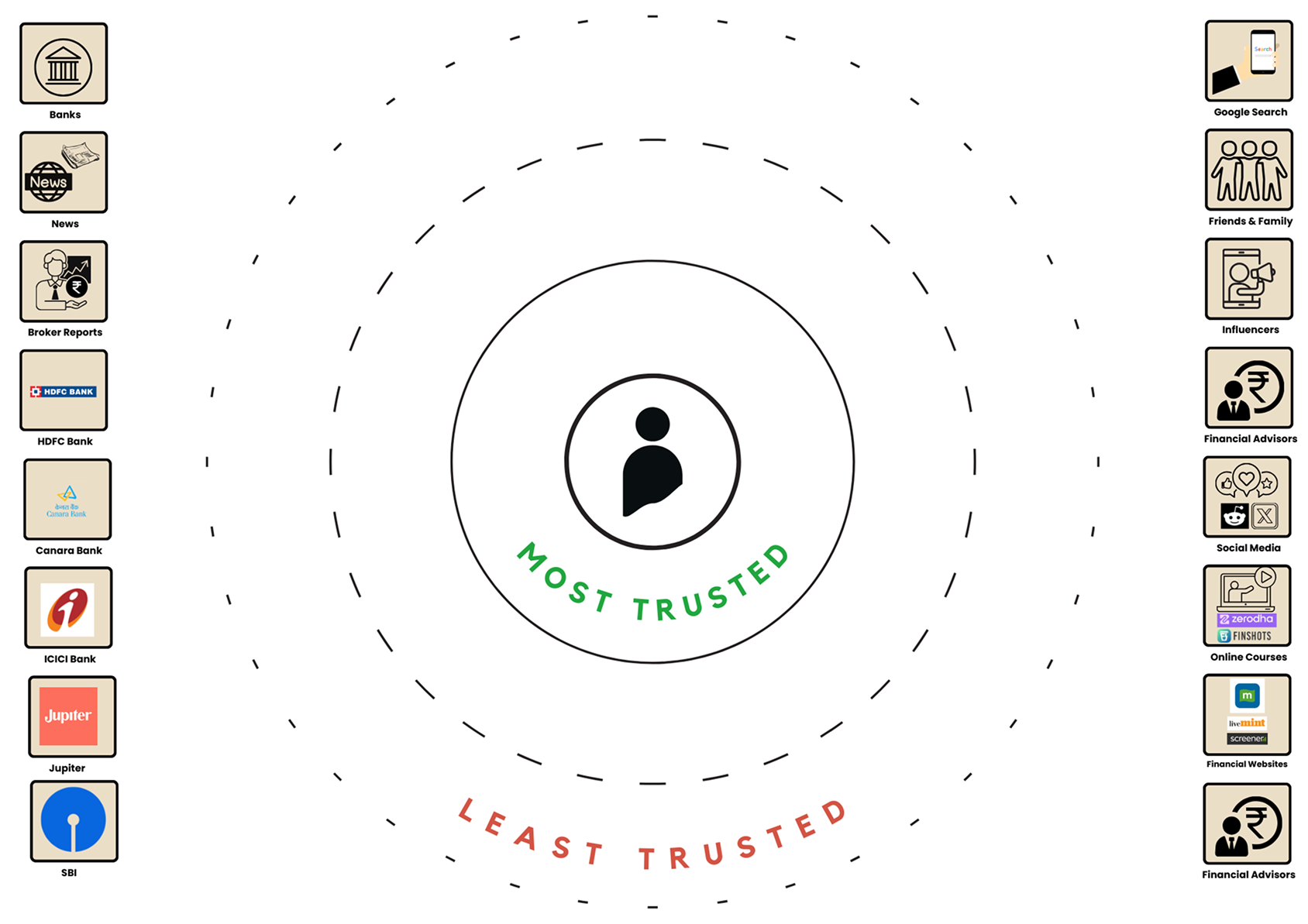

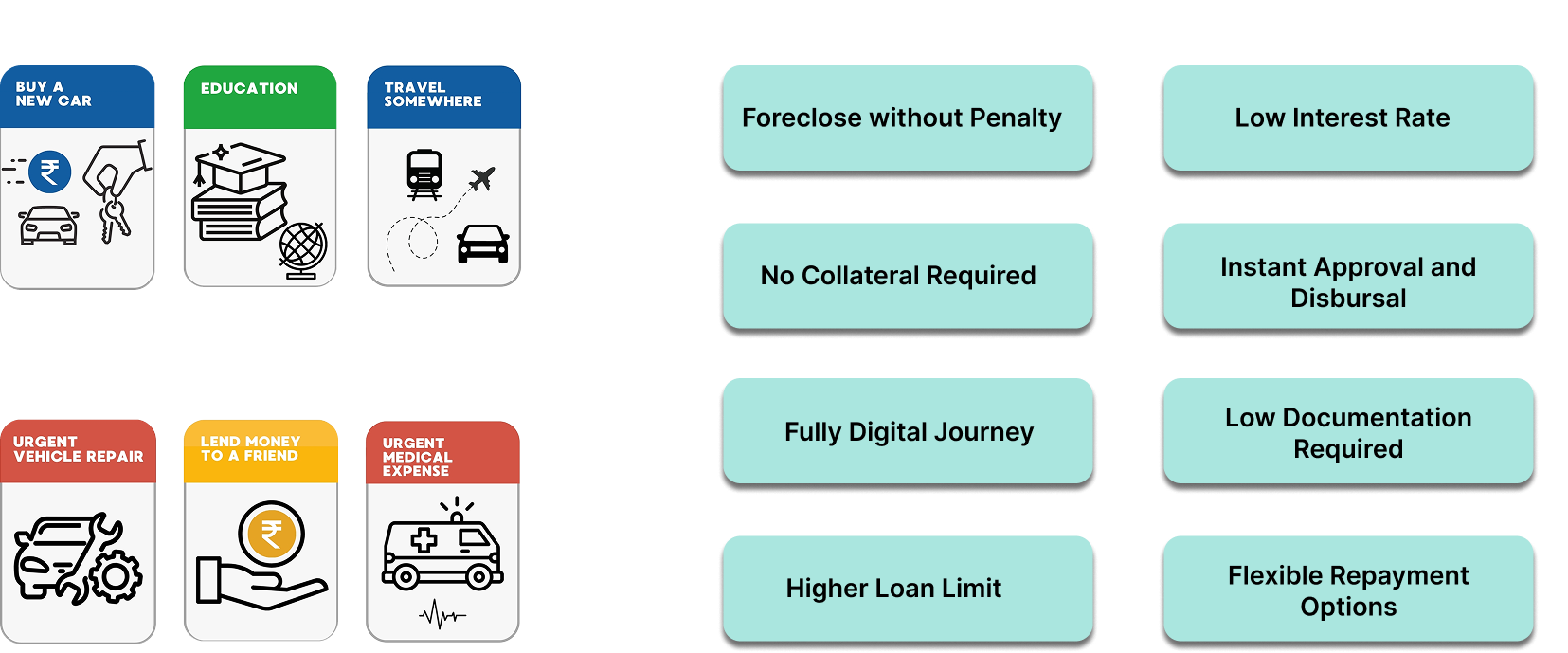

Unlike traditional research methods, we employed a discussion guide that involves in-depth qualitative interviews supplemented by interactive activities to explore Gen Z’s financial behaviours, decision-making processes, and trust in financial systems. The approach combines behavioural probes, scenario-based exercises, and hands-on financial simulations to extract insights beyond stated preferences.

The study utilizes a mix of visual, interactive, and narrative-based exercises designed to uncover motivations, preferences, and barriers in financial decision-making. These include: